Portfolio Access

Portfolio Access Bond Trading

Bond Trading

Related Articles

1. The Recent Market Drop: Unpacking the Numbers

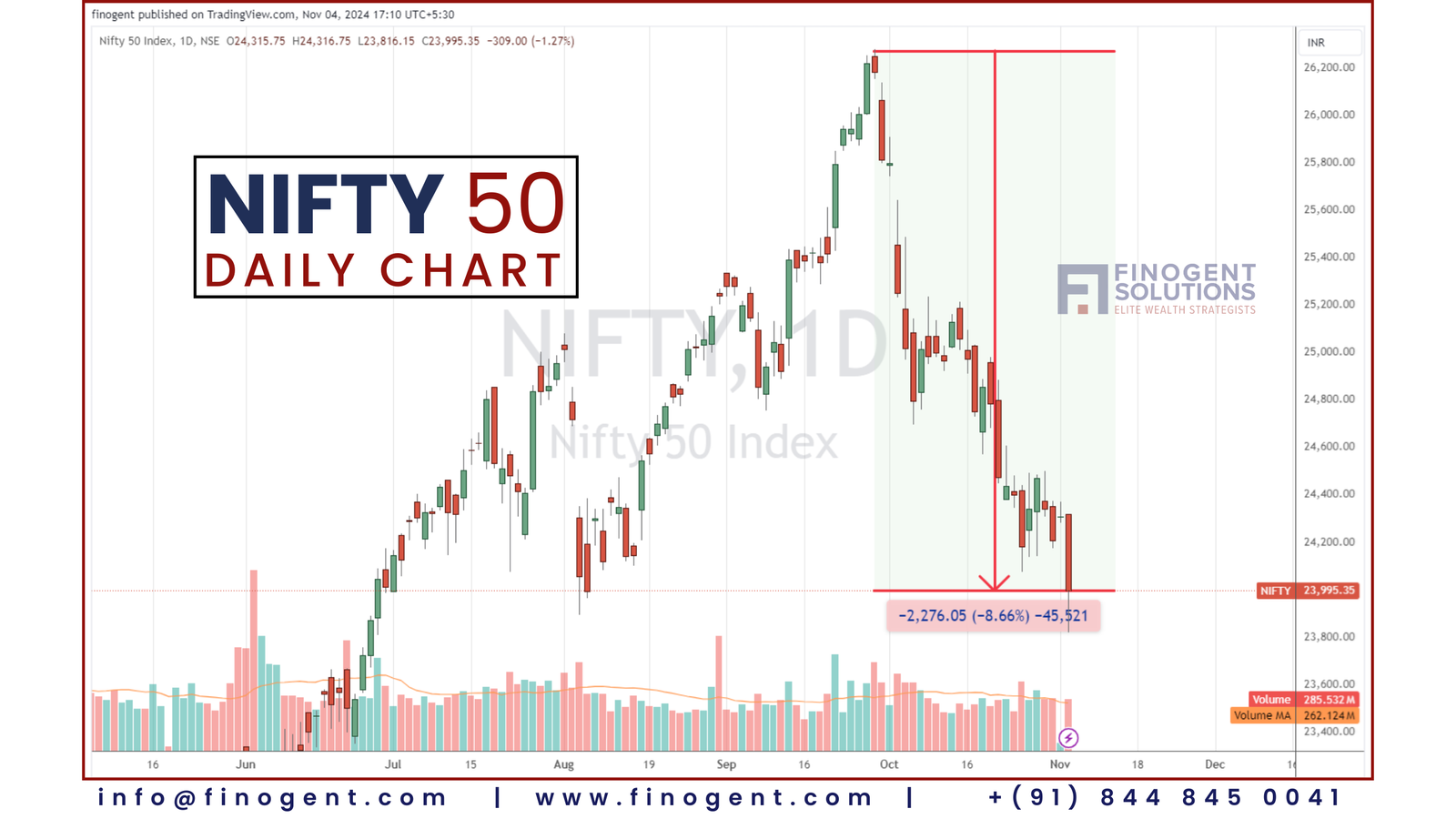

The Nifty index experienced a sharp decline, marked by an 8.66% fall since the end of October. This stark drop was visible on the daily charts, where a prominent red candle highlighted the sell-off. The immediate impact was widespread, with major sectors and large-cap stocks experiencing significant losses.

This decline broke the momentum-driven optimism many investors had, reminding us that stock market returns are cyclical.

This was not the first time that the markets fell this much; however the difference the steep fall had happened within a month; as here I would show you 3 other instances where we have seen NIFTY50 falling and the fall had stretched over the quarter; and all these main corrections had been over the Sep – Dec Quarter which in certain cases stretched to March Quarter.

The recency bias, where investors assume that recent trends will continue indefinitely, led to unrealistic expectations. Many were accustomed to returns of 20-40% annually, without considering that such periods are typically followed by corrections or periods of stagnation.

2. Global and Domestic Factors at Play

Key Influences that led to the decline:

- U.S. Federal Reserve Policy & US Elections: The anticipation of the Fed’s upcoming interest rate decision on November 6th has kept global markets on edge. The potential rate cuts or status quo could significantly impact not only U.S. markets but also ripple into the Indian financial landscape; compounded by US elections.

- China’s Stimulus Plans: Investors are closely watching China’s National Party Congress for cues on economic stimulus. A large-scale stimulus could redirect foreign investment flows toward China, impacting the Indian market.

- Foreign Institutional Investors (FII) Behavior: Recent FII selling, driven by global uncertainties, has contributed to the negative sentiment in Indian equities.

These influences, among others, create a complex environment where market behavior is not just a reaction to domestic factors but a blend of global economic policies and investor sentiment.

3. Dispelling the Myth: Defensive Sectors Aren’t Always Defensive

Conventional wisdom suggests that during market downturns, sectors like FMCG and Pharma act as safe havens. However, recent data has proven otherwise. The FMCG sector, for instance, fell by approximately 11.5%—outpacing the overall decline of the Nifty.

This fall can be attributed to subdued demand, both in urban and rural areas, coupled with rising cost factors pressuring profit margins.

It is a crucial reminder that no sector is immune, and investors must evaluate underlying fundamentals before considering any sector as a cushion during turbulent times.

4. Sectoral Analysis: Winners and Losers

Top Performers:

- IT Sector: Surprising many, the IT sector has outperformed due to its global client base, making it less susceptible to domestic volatility.

- Pharma and Services: These sectors have shown relative strength compared to broader market indices.

Lagging Sectors:

- Energy and Auto: Companies like Coal India, NTPC, and major auto manufacturers have struggled, primarily due to structural challenges and inventory issues.

- Metals and Infrastructure: These sectors have been hit hard, mirroring the broader market decline.

Investors can consider dividend-paying stocks within these lagging sectors to benefit from better yields during downturns.

5. Nifty vs. Mid-Caps, Small-Caps, and Micro-Caps: A Comparative Analysis

During periods of market volatility, it is commonly believed that large-cap stocks, such as those in the Nifty 50, are more stable and resilient compared to mid-cap, small-cap, and micro-cap stocks. However, a deeper examination of recent trends challenges this notion and provides fresh insights into how these segments perform relative to each other during market corrections.

Performance Overview

From mid-September to early November 2024, we observed that the Nifty 50 experienced a decline of approximately 8.66%. When comparing this with the mid-cap, small-cap, and micro-cap indices, notable differences emerged:

- Mid-Cap Index: The mid-cap index showed a lesser decline, around 4.5% to 4.71%, indicating that while it was impacted, the fall was less severe than that of the large-cap Nifty 50.

- Small-Cap Index: The small-cap index experienced similar behavior, demonstrating resilience by falling less than the Nifty 50.

- Micro-Cap Index: The micro-cap index initially saw a sharper drop, but it also displayed strong recovery capabilities, often bouncing back more rapidly than its larger counterparts.

Key Insights:

- Volatility and Recovery: While mid-cap, small-cap, and micro-cap stocks are typically perceived as more volatile, they can show quicker recoveries post-decline. This behavior highlights that although these segments may react strongly to market news, their rebound potential can sometimes surpass that of larger indices.

- Diversification Benefits: The broader stock base available in the small-cap and micro-cap indices provides opportunities for more democratic and diversified investment choices, potentially buffering against prolonged downturns in large-cap-heavy indices like the Nifty 50.

6. The Importance of Diversification and Asset Comparison

A comprehensive understanding of how different asset classes perform during volatile periods is crucial for creating a balanced investment strategy. Analyzing Nifty’s performance alongside other key asset classes such as gold, global equities (e.g., NASDAQ), and regional benchmarks (e.g., Hang Seng) provides valuable insights into diversification benefits and risk management.

Performance Breakdown from January 2023 to November 2024

- Nifty 50: Despite recent volatility and a sharp 8.66% decline observed since late October 2024, the Nifty 50 has still managed to deliver a cumulative return of approximately 31% from January 2023 to November 2024.

- NASDAQ: In contrast, the NASDAQ index has significantly outperformed, boasting a return of approximately 81.55% over the same period. This steep performance highlights the continued strength of U.S. technology and growth stocks, driven by resilient corporate earnings and robust global demand.

- Gold: Known for its status as a safe-haven asset, gold has delivered a more moderate return of around 36% during this timeframe. While it hasn’t matched the NASDAQ’s explosive growth, its steady appreciation underscores its role as a stabilizer during market uncertainties.

- Hang Seng Index: The Hang Seng has shown a return of approximately 18.9%, influenced by China’s economic policies and recent stimulus efforts aimed at revitalizing growth. This uptick reflects investor optimism in the region, but with inherent risks tied to geopolitical and economic shifts.

Key Takeaways for Investors:

- Diversification is Essential: The wide variance in returns across different asset classes emphasizes the importance of diversification. While Nifty 50’s performance remains commendable, having exposure to global equities and commodities like gold can enhance a portfolio’s resilience.

- Balancing Growth and Safety: The NASDAQ’s strong performance illustrates the potential of growth-oriented investments, while gold’s steady gains serve as a reminder of the importance of having assets that can act as a safety net during market downturns.

- Emerging Opportunities: The recent recovery in the Hang Seng index signals potential in diversifying into Asian markets, especially when geopolitical and economic conditions are favorable.

Strategic Perspective

Investors who focus solely on domestic equities like the Nifty 50 may miss out on broader growth opportunities or the stability that comes from strategic diversification. The NASDAQ’s high returns signal the value of incorporating global equities, particularly technology, into one’s portfolio, while gold’s modest but reliable performance confirms its role in hedging against market corrections. The Hang Seng’s recent gains also point to the importance of staying attuned to regional economic shifts that can open new avenues for growth.

7. Opportunities in REITs and Alternative Investments

Real Estate Investment Trusts (REITs) have gained attention as an alternative asset class that provides a blend of stability and income, especially during volatile equity market phases.

In our analysis, we observed the performance of notable REITs like Embassy Office Parks, Brookfield, and Mindspace have shown capital gains between 3.5% to 6%, along with consistent dividend payouts.

Performance Metrics

As of September 27, 2024, the stock market had experienced a decline of approximately 8.66%, as discussed earlier. However, during this same period, REITs demonstrated resilience:

- Capital Appreciation: The value of REITs showed a gain ranging from 3.5% to 6% during the market downturn. This capital appreciation highlighted their capacity to counterbalance some of the losses from traditional equities.

- Dividend Yield: REITs are legally required to distribute 80-90% of their income as dividends, making them a reliable source of passive income. For instance, yields can be in the range of 6% annually, which adds to their attractiveness as a portfolio stabilizer.

For investors seeking stability, real estate investment trusts (REITs) have proven to be a viable option.

Why Consider REITs?

- Hedge Against Volatility: The relatively stable performance of REITs compared to the sharp decline in broader equity markets underscores their role as a potential hedge in times of market stress.

- Income Consistency: Beyond capital gains, the mandatory dividend payouts ensure investors benefit from regular income, making REITs appealing for those looking for cash flow during uncertain times.

- Opportunity During Declines: Periods of market correction, such as in 2023 when REIT prices dropped significantly, present opportune moments to enter or expand positions. These lower prices increase the dividend yield potential and set the stage for potential capital appreciation as the market recovers.

Strategic Takeaway

Incorporating REITs into an equity portfolio can provide dual benefits: a buffer against extreme market movements and consistent income generation. While traditional equities, such as those in the Nifty 50, may face periods of substantial volatility, REITs have shown the ability to perform more steadily, balancing out the risks. Investors seeking to diversify their holdings and mitigate downturn impacts should evaluate REITs as a viable component of their long-term strategy.

8. Strategic Steps Forward

Current market developments and turmoil has provided investors with an opportunity to do the reality check and re-structure the strategy:

Investors should follow 3 things:

- Adopt a Value-Based Strategy: Transitioning from momentum investing to value-based stock selection can better align with the current market dynamics.

- Tax Loss Harvesting: Leverage the current downturn to book unrealized losses, offsetting gains and reducing tax liabilities while freeing up capital for reinvestment.

- Psychological Preparation: Approach the market with a long-term mindset. The expectation of consistent, high annual returns is unrealistic; understanding market cycles is essential for sustained investment success.

Conclusion

Markets will continue to cycle through periods of growth and correction. As investors, aligning your strategy with the prevailing market dynamics, managing expectations, and maintaining a diversified portfolio are key to navigating these cycles successfully. Remember, investing is a marathon, not a sprint.

Disclaimer:

This blog post is for informational purposes only and should not be considered as financial or investment advice. The analysis and opinions expressed are those of the author, Rajat Dhar, and do not necessarily reflect the views of Finogent Solutions LLP. Investors are encouraged to conduct their own research and consult with a financial advisor before making investment decisions. Past performance is not indicative of future results.